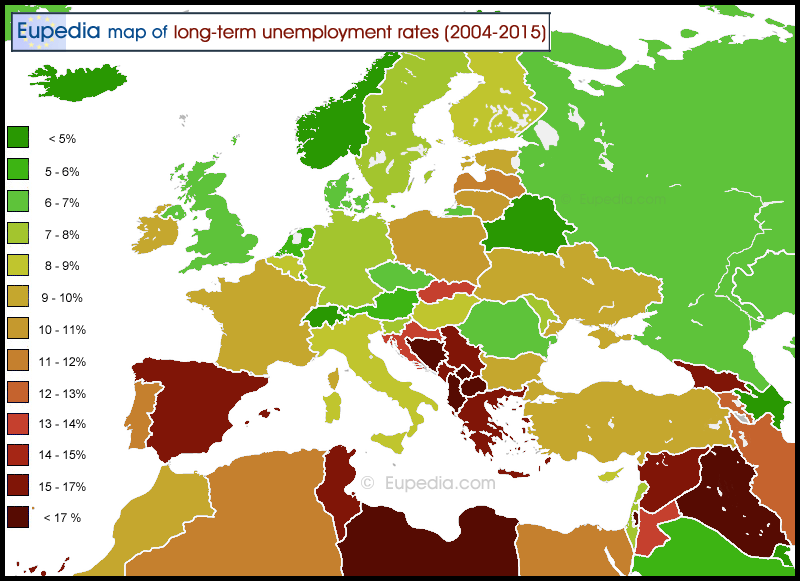

I have been making

socio-economic maps for several years. Here is the latest addition. I have calculated the average unemployment rates for the 12-year period 2004-2015. Unemployment rates change all the time and it is only useful to compare the economic health of countries based on data spanning many years.

Note that some countries suffered much more than others from the 2008 financial crisis in terms of unemployment rates. Some countries were badly hit by the crisis but have recovered quite well (Ireland, UK, Czech Republic, Latvia, Lithuania, Cyrpus), while others were slower to recover (Portugal, Spain, Croatia, Slovakia, Greece). Some countries were mostly unaffected by the crisis in terms of employment at least (Iceland, Norway, Belgium, France, Switzerland, Austria, Slovakia, Romania), and some actually performed better since the crisis (Germany, Poland). In Italy and the Netherlands, unemployment started increasing noticeably only since 2012, 4 years after the crisis. Unemployment only rose by a few points after 2008 in Denmark and Sweden, but they haven't really recovered yet.

Data for countries like Belarus (officially around 1% unemployment for years), Russia and Azerbaijan (sudden drop from 16% to 1% in a single year) should be taken carefully, as these countries may cook up their numbers.

Can you explain a bit more why France is mostly unaffected by the crisis in terms of employment at least?

I don't think French economy is doing well, especially up north and amongst the youth. The jihadist attacks in Nice and the murder of a priest in northern France in July, which led to a significant fall in tourism were partly responsible for jobless increase in France.

According to this website:

http://fortune.com/2013/01/09/the-euro-crisis-no-one-is-talking-about-france-is-in-free-fall/

In the boom years of the mid-2000s, France virtually matched Germany as the twin growth engine of the thriving, 17-nation eurozone.

A deeper look shows that France is mired in no less than an economic crisis. The eurozone’s second-largest economy (2012 GDP: 2 trillion euros) is suffering more than any other member from a shocking deterioration in competitiveness. Put simply, France’s products -- its cars, steel, clothing, electronics -- cost far too much to produce compared with competing goods both from Asia and its European neighbors, including not just Germany but even Spain and Italy. That’s causing a sharp and accelerating fall in its exports, and a significant decline in manufacturing and the services that support it.

The virtual implosion of French industry is overlooked by analysts and pundits who claim that the eurozone had dodged disaster and entered a new, durable period of stability. In fact, it’s France -- not Greece or Spain -- that now poses the greatest threat to the euro’s survival. France epitomizes the real problem with the single currency: The inability of nations with high and rising production costs to adjust their currencies so that their products remain competitive in world markets.

So far, the worries over the euro have centered on dangerously rising debt and deficits. But those fiscal problems are primarily the result of a loss of competitiveness. When products cost too much to make, the economy stalls or actually declines, so that even modest increases in government spending swamp nations with big budget shortfalls and excessive borrowings. In this no-or-negative growth scenario, the picture is usually the same: The private economy shrinks while government keeps expanding.

That’s already happened in Italy, Spain and other troubled eurozone members. The difference is that those nations are adopting structural reforms to restore their competitiveness. France is doing nothing of the kind. Hence, its yawning competitiveness gap will soon create a fiscal crisis. It’s absolutely astonishing that an economy so large, and so widely respected, can be unraveling so quickly.

The world’s investors and the euro zone optimists should awaken to the danger posed by France. La crise est arivée.

France’s decline is best illustrated by the rapid deterioration in its foreign trade. In 1999, France sold around 7% of the world’s exports. Today, the figure is just over 3%, and falling fast. The same high costs that are pounding exports draw an ever rising flow of goods from Germany, China and even southern Europe. Those imports are taking an increasing share of sales from pricier French-made products. In 2005, France’s trade balance was a positive 0.5% of GDP. Today, it stands at minus 2.7% of national income, meaning imports now far exceed exports, turning trade from a growth-generator into a major drag. An excellent illustration of the competitiveness gap is the chasm between German and French exports to China. Germany sends $70 billion in cars, machine tools and other products to China each year, seven times the figure for France.

Even tourism is suffering because of the France’s high prices. France is now struggling to attract clientele from a surging, bargain-seeking tranche of the market, travelers from Asia, Brazil, India and Russia. In the mid-2000s, foreigners spent 15 billion euros more visiting the Champs Elysees and the Riviera than the French paid to vacation abroad. That surplus has since fallen by one-third, to around 10 billion euros.

The main reason for France’s cost disadvantage is the burden of labor, a factor that typically accounts for around 70% of all corporate expenses worldwide. In France, the problem comprises high wage and social costs, and rigid laws, including a 35-hour work week that allows French employees the lowest number of working hours in the developed world. An astounding 86% of all wage earners enjoy “contrats a durée indéterminées,” permanent contracts that make layoffs extremely expensive and time-consuming.

In France, 42 euros for every 100 euros in total expenses go to social charges, versus 34 euros in Germany, 26 in the UK, and 20 in the US.

Obviously, the restrictive laws and hostile unions are nothing new. What’s causing the crippling malaise is the recent rapid rise in labor costs when rivals are lowering or moderating the weight of their workforces.